The Market for Control: An Overview of the Private Cloud Services Market

The global push for digital transformation, coupled with persistent concerns about security and data sovereignty, has created a massive and enduring market for dedicated cloud infrastructure. The global Private Cloud Services Market is a large and steadily growing ecosystem of hardware vendors, software providers, and managed service specialists dedicated to building and operating single-tenant cloud environments. This market offers a compelling alternative to the public cloud for organizations that require greater control, security, and customization. Driven by the needs of regulated industries, the performance requirements of critical applications, and the rise of hybrid cloud strategies, the private cloud remains a fundamental and strategically important component of the overall cloud computing landscape, creating a huge and competitive market for the vendors who power it.

To better understand its structure, the market can be segmented by its core service types, the size of the organization it serves, and the end-user industry. By service type, the market is broadly divided into Infrastructure as a Service (IaaS), which provides the raw compute, storage, and networking resources; Platform as a Service (PaaS), which offers a platform for developing and deploying applications; and Software as a Service (SaaS), where specific applications are delivered from a private cloud environment. The market is also segmented by organization size, with solutions tailored for large enterprises with complex needs being the dominant segment. By industry, the market sees its heaviest adoption in sectors with high security and regulatory requirements, such as Banking, Financial Services, and Insurance (BFSI), healthcare, government, and defense, but it is also widely used by retail and manufacturing companies for their mission-critical applications.

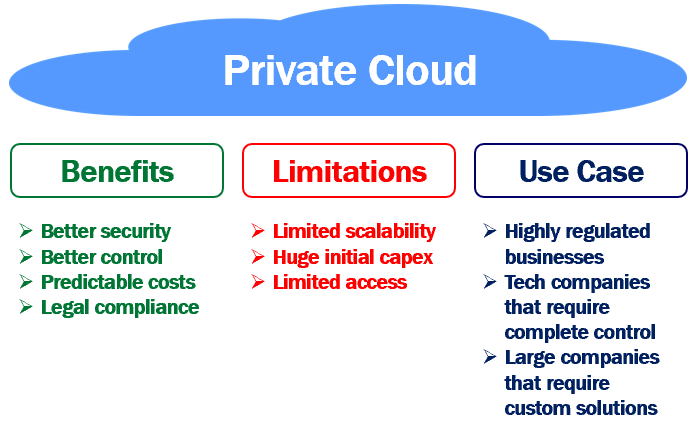

The primary forces propelling the market's continued expansion are powerful and rooted in the practical realities of enterprise IT. The number one driver is security and compliance. For many organizations, the perceived or real security risks and the lack of control in a multi-tenant public cloud are unacceptable for their most sensitive data and critical applications. A private cloud provides the isolation and control necessary to meet strict regulatory mandates like GDPR, HIPAA, and PCI DSS. Another major driver is application performance and customization. Certain legacy or high-performance computing (HPC) applications may have specific hardware or network requirements that are difficult or impossible to meet in a standardized public cloud environment. A private cloud allows for complete customization of the underlying infrastructure to optimize performance for these critical workloads.

Despite the strong growth of the public cloud, the private cloud market continues to thrive because it addresses key challenges. However, it is not without its own set of hurdles. The primary challenge of a self-managed private cloud is the high upfront cost (CapEx) and the complexity of building and operating it. It requires significant investment in hardware and a highly skilled team of engineers. This is why the "managed private cloud" model has become so popular, as it offloads this burden. Another challenge is the perceived lack of agility compared to the public cloud. While a private cloud is far more agile than a traditional data center, it typically cannot match the instant, on-demand scalability of a hyperscale public cloud provider. This has led to the rise of hybrid cloud strategies, where companies use a mix of private and public clouds to get the best of both worlds.

Top Trending Reports: